GAP Requirements

July 1, 2020

By: Michael J. Dommermuth and J. Randolph Earnest

The Colorado Attorney General's office recently launched an investigation of GAP, in Colorado. At least 10 GAP Administrators were served with subpoenas purporting to require extensive production of information and documents. At this time it appears that no dealers are the target of this investigation, however it is a good time for a refresher concerning GAP requirements in Colorado.

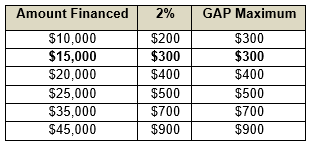

In Colorado, GAP is typically a debt cancellation product and it is regulated by the Uniform Consumer Credit Code. The Colorado Uniform Consumer Credit Code adopted Rule 8 which specifies rate caps for GAP contracts. The GAP fee may not exceed $300 or 2% of the amount financed, whichever is higher. Those fees are summarized in the following chart.

In addition, the GAP contract must conspicuously disclose the following items:

- That purchase of GAP is not required in order to obtain credit or any particular favorable credit terms;

- The fee or premium for the GAP;

- The consumer may wish to consult an insurance agent to determine whether similar coverage may be obtained and at what cost;

- The GAP benefits may decrease over the term of the consumer credit sale or consumer loan;

- The consumer may cancel GAP for any or no reason within 30 days after GAP was purchased and receive a full refund of the GAP fee or premium so long as no loss or event covered by GAP has occurred; and

- GAP is not a substitute for collision or property damage insurance.

The GAP contract must also include the following language:

IF THIS TRANSACTION CONTAINS A FEE OR PREMIUM FOR GUARANTEED AUTOMOBILE PROTECTION, ALL HOLDERS AND ASSIGNEES OF THIS CONSUMER CREDIT TRANSACTION ARE SUBJECT TO ALL CLAIMS AND DEFENSES WHICH THE CONSUMER COULD ASSERT FROM THE CONSUMER’S PURCHASE OF GUARANTEED AUTOMOBILE PROTECTION.

Consumers are entitled to a pro-rata refund of the GAP charges if the underlying loan is prepaid prior to maturity or the vehicle is no longer in the consumer’s possession due to repossession and no GAP claim has been made.

Finally, Colorado regulations require that the dealer provide a separate written cancellation form at the time of consummation of the GAP contract.That document:

- must include the name and mailing address to be used to cancel GAP;

- must state clearly and conspicuously that the consumer has the unconditional right to cancel GAP for a full refund within 30 days after it was purchased; and

- state that in order to cancel GAP the consumer must complete and return the form or send any other written notice of cancellation to the address provided, postmarked no later than 30 days after the GAP was purchased.

At the time of purchase, the consumer must also be provided with:

- the GAP insurance policy, certificate, or written description of GAP’s benefits;

- terms, conditions, and exclusions; and

- the procedure and timing to be followed to make a claim after a total loss.

Dealers should retain a copy of all the GAP documents provided to the consumer in the deal jacket, including, but not limited to the unsigned written cancellation form provided to the consumer. The UCCC occasionally audits dealers and requires proof of a cancellation form in the deal jacket to verify compliance.

This is a good time to review your GAP products for compliance Colorado law. Audits of GAP administration companies can lead to audits of dealers!

* GAP is more commonly known as Guaranteed Asset Protection but Colorado’s Rule 8 refers to it as Guaranteed Automobile Protection.